Cronos Group Update: A multi-bagger in the making?

And some brief thoughts on Organigram, the broader industry, and capital cycles

Disclaimer: Nothing on this blog is intended as financial or investing advice. Please do your own due diligence.

“The Canadian market has been characterized by extreme cycles of supply, demand imbalances. In the early days of legalization, there was not enough supply to meet demand… This placed a lot of industry focus on facility size, not on production efficiency or product quality. As a result, total supply quickly ballooned and significantly outpaced demand. The industry structure and expectations were all set up with price assumptions that were 3 to 4 times what they are today and that created a market structure with high excise tax, high provincial margins and high regulatory fees.

However, companies with inefficient production facilities, having already built significant capacity, had to capture significant market share for their business models to work, and attempts to get that market share led to price compression. Many of these companies continue to raise capital, albeit on much less attractive terms and hopes to survive long enough to benefit from expected tailwinds of attractive international markets opening or rationalization in the Canadian market…. However, with global macro events taking priority with policymakers, many producers were not able to survive long enough to see benefits of new markets opening….

Over the last year, we have seen CRA begin to ramp up collections and enforcement against companies not paying excise tax and regulators crackdown against lab shopping, forcing more facility shutdowns and bankruptcies. And earlier this year, with regulatory changes in Germany and increased traction in the UK, we've seen international demand finally begin to ramp…”

— Cronos Group CEO, Mike Gorenstein during the Q2 2024 Earnings Call

***

Although you wouldn’t know it from the share price (shares are up ~20% since my original write-up in March), the underlying Cronos thesis is unfolding with more force and speed than I ever imagined. Though we remain in the second inning of the long-term story, I believe last week’s Q2 earnings release, in addition to some of the broader developments in the industry, warrant a brief update.

[As some of you know, I am now expressing this cannabis theme through a combination of Cronos and Organigram (OGI). Though I have not explicitly pitched the latter, the stories are so similar — dominant LPs, fundamentals moving in parallel, big tobacco backing (BAT will soon own ~45% of OGI, akin to Altria’s +40% interest in CRON) — that I am largely treating them as the same trade and will discuss them in tandem.

Ultimately, the difference for me comes down to the balance sheets; while CRON’s $800m war chest of cash provides it with a huge margin of safety and attractive optionality if and when it gets deployed, it is a massive drag on the equity for the time being; OGI, on the other hand, though also in possession of material net cash, offers a lot of more torque as its cash pile is a far small portion of its total market cap.

I find both these opportunities similarly compelling and, combined, they represent the second largest position in my portfolio behind Cipher.]

Cronos’ Q2 results last week were extremely impressive. Here are the takeaways (in $USD):

Net Revenue (i.e. sales less excise tax) grew 46% YoY to $27.8m;

Gross margin improved 700 bps to 23%;

EBITDA, though still negative, improved 31% to -$11m;

Cash flow from operations was positive $1.7m vs. -$11.8m YoY, and is approximately breakeven YTD;

Cash declined slightly due to investments in GrowCo, but would otherwise have increased, and is still a whopping ~$800m;

Spinach continues to grow and dominate, with a ~16% share in edibles;

Further investments were made in GrowCo (which will now be consolidated) providing a lot of strategic value that is being overlooked.

I want to double-click on a few of these items, starting with 46% net sales growth. This is now squarely a growth stock. What’s going on?

One might think, given Gorenstein’s comments above on capital cycle dynamics, that the industry is rapidly reaching price rationalization. But while the trend is clearly towards rationalization, material improvements in pricing have yet to be felt and cannabis prices in Canada remain very depressed (see e.g. here). And in fact, though pricing on flower appears to have stabilized, Cronos’ update explicitly notes that its sales were negatively impacted by price mix. Therefore, topline growth appears to be coming entirely from volume increases. And that growth is both in flower and extracts, and importantly, is principally driven by domestic Canadian sales:

While the broader Canadian market is certainly growing volumes (industry revenues have grown at a ~30% 5-year CAGR despite collapsing prices), it’s clear that much of the company level growth is being achieved by capturing incremental market share.

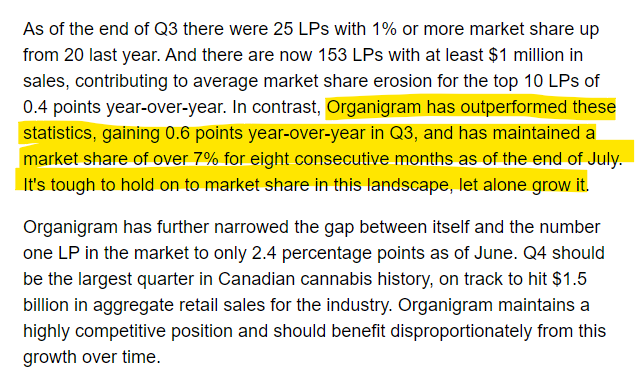

Here’s OGI’s CEO Beena Goldenberg, noting OGI’s success notwithstanding increased competition from LPs:

We know Cronos experienced similar gains in market share, given Spinach has now become the #1 selling flower in Canada, while increasing its domination in other categories as well (including 16% in the higher margin edibles category).

Growing market share in the face of irrational industry behavior and fierce competition is, alone, impressive; doing so whilst drastically slashing costs is magical. Cronos has done just that, remarkably slashing opex from 92% of gross sales to 56% of gross sales in just one year, including an absolute reduction in sales and marketing expense of ~18%. (OGI has accomplished similar results).

How is this possible? Well, I’d posit that a couple things are happening:

The Emergence of Brand Power

You simply don’t see market share capture happen with a commoditized offering concurrent with reduced S&M expense and increased competition unless you’ve built a brand. Cronos has done just that with Spinach, which continues taking market share in seemingly every category quarter after quarter.

Anecdotally, if you walk into many Canadian dispensaries, as I have, you will see a multitude of products on the shelves, but one brand will clearly catch your eye for how ubiquitous it seems to be, and that’s Spinach.

As I’ve discussed before, cannabis’ predecessor industries, beer and tobacco, were once commoditized products in irrational industries that evolved to become dominated by oligopolies with brands powerful enough to distract from the fact that the underlying product is still very much a commodity. (See e.g. here and here). We are seeing this phenomenon in embryonic form with cannabis today.

On this front, I’d note that due to its first-mover advantage and the curtailing of R&D spend in the US due to section 280E, the Canadian LPs are well ahead of their US counterparts in developing brands (which attach better to specialty products like edible and vapes, than to flower) — a competitive advantage that will only be augmented by our big tobacco backers.

Prudent and aggressive investments are starting to pay off

Here’s Goldenberg again on how investments are leading to increased plant yields, manufacturing efficiency, and ultimately fixed cost leverage (Cronos is clearly experiencing similar efficiency gains, which should continue to increase, e.g. through the further investments in GrowCo):

Together, the CRON and (equally impressive) OGI updates have led me to a firm conclusion: these are high growth businesses carving out very material competitive advantages, and inflecting towards profitability. And they are achieving all of this within an industry that remains completely irrational and viciously challenging.

I’d encourage readers to now consider two things: 1) what happens when consolidation inevitably comes and they can actually start taking more price?; and 2) what happens when the excise tax, which is still capturing a preposterously punitive ~1/3 of sales, gets reformed?

The answer is clear: they are going to be cash flow gushing juggernauts.

Indeed, simply removing the excise tax and keeping all else constant, Cronos’ run-rate EBITDA would be ~$45m, which would put this at essentially 2x EV/EBITDA. And again, that accounts for no further topline growth or margin expansion, both of which will explode the minute we start seeing prices increase.

And I have very little doubt that those two conditions will the be reality sooner than later.

On the first, consolidation, I’d note that insolvencies continue to swell as many uneconomic players are increasingly forced to the exits. This is being propelled by the Canada Revenue Agency increasingly cracking down on market participants that have failed to pay outstanding excise taxes, a figure which is now estimated to be CAD~$270m.

Which brings me to the second point, the excise tax itself. I spent a lot of time discussing how ridiculous this tax is in my original piece on CRON. My thoughts are largely unchanged, and although the Trudeau government (unsurprisingly) declined to reform the tax in April, I’d just reemphasize that a) it is completely disproportionate when juxtaposed against the levies faced by alcohol and tobacco industry participants; b) reforming it would be an easy way to score points for a new Parliament (I’m looking at you Pierre); and c) perversely, the longer the tax is kept in place, the quicker we will achieve rationalization.

Looking Ahead - Multi-Baggers in the Making (Many Times Over??)

If you asked me to identify the stocks I think are mostly likely to be 10-baggers a decade from now, my answer today would be CRON and OGI. In fact, call me crazy, but I think there’s an outsized shot at a 100-bagger upside to these enterprise values over the long-term. I really believe that. While Cronos’ $800m of cash impedes a 100x outcome from being practical at the moment, OGI currently boasts a market cap of ~$200mUSD — is $20B for a global blue chip cannabis player a decade or two out possible? I think very much so, and here’s why.

A massive growth runway.

We’ve already discussed the impressive topline growth currently being achieved. But this is just scratching the surface.

a) Pricing Upside

For one, as discussed, cannabis prices remain extremely depressed in Canada. In fact, cannabis might be the only item I can think of that has actually seen material price deflation in recent years; compared to the punishing inflation felt across virtually every other good and service, I honestly can’t think of anything in Canada offering better “bang for your buck” than cannabis. Seriously: how about 28 grams of flower for ~$55USD? (For those of you not familiar with consumption in practice, 28 grams (1 ounce) could get you feeling pretty good every night for several months!) For further perspective, you would have been hard pressed to purchase even half an ounce for less $100 a decade ago on the illicit market. That’s how rock-bottom prices currently are.

All that is to say: when prices do get rational (and that time will come) they will go a lot higher. Moreover, I suspect prices could double or more before we see any material demand elasticity. Indeed, we likely see both volumes and prices increase in tandem at some point soon.

b) Market Growth

In addition to upside from pricing, the market itself is still growing.

By one estimate, the Canadian cannabis market is expected to grow 3% through to 2030 to a size of $6.5B USD. Assuming Cron captures 5% of that market ($325m of gross sales), that would effectively result in Cronos doubling its top line by decade-end just on its Canadian book of business (i.e. ignoring very material contributions from Israel and ROW). Laughably, $325m is more than 3x CRON’s current enterprise value.

c) International Expansion

And of course, that’s just the Canadian opportunity, which pales in comparison to the global opportunity. I won’t rehash my thinking on this (see my original write-up), but I am more confident than ever that CRON and OGI are the best positioned companies in the world to seize on this opportunity, given their: early mover advantages, substantial in-roads already made internationally (e.g. Israel, Germany, Australia, UK), and unique access to big tobacco’s global distribution and marketing networks and cheap relative cost of capital.

Just consider the US opportunity alone, which is currently projected to be worth $100B by the end of the decade and nearly the same size as tobacco:

And as I have argued before, no one is an a better position to capture market dominant market share in the US than CRON and OGI given their relationships with Altria and BAT, who are both explicitly positioning themselves to capitalize on this opportunity upon legalization through these entities.

If the US landscape shapes into an oligopoly down the road as beer and tobacco have — (and why would it not?) — and CRON and OGI are part of that oligopoly — (Altria and BAT would have it no other way) — then we are looking at companies that could be generating billions of dollars in annual sales in the future.

Indeed, large US players like CURLF are already generating >$1B in sales and 1) cannabis isn’t even federally legal yet - CURLF only operates in 19 states and 2) they don’t have distribution, marketing and R&D infrastructure remotely on par with that of Big Tobacco’s. It shouldn’t be hard for CRON and OGI to hit $1B in sales once you factor in their Canadian segments alone should be doing several hundred million in no time.

A lot admittedly needs to happen before this angle comes into play, but it’s a call option that should be worth a lot more than the zero it is currently being ascribed.

Margin expansion

On top of all this growth, we have enormous opportunity for margin expansion given the inherent operating leverage these businesses have demonstrated as they’ve scaled. That leverage will really start to explode once prices rationalize. And of course, there’s the margin upside that simply comes from eliminating the excise tax: e.g. Cron’s gross margins would be closer to 42%, rather than 23%, absent the excise tax (OGI’s even higher).

(Re)Investment Opportunity

This is another common multi-bagger characteristic that these companies possess.

Equipped with armories of cash and huge cost of capital advantages, CRON and OGI have the ability to accretively deploy enormous amount of capital within an industry with depressed valuations and an abundance of growth and strategic opportunities on offer. I expect continued international expansion, further strategic investments into product development and cost efficiencies, and potential M&A to expedite industry consolidation.

With the market currently ascribing minimal value to the enterprise, the hurdle to deploying the cash in a value additive manner is extremely low.

Competitive Advantages

I won’t reiterate these here yet again, except to say that I think the market is utterly overlooking some very significant competitive advantages.

Multiple Expansion

And the final piece to the multi-bagger equation: (a lot) of room for multiple expansion.

There are too many unknowns and the fairway is too wide for any modelling exercise to even matter, but I look at it this way. Both CRON and OGI have enterprise values less than 1x NTM sales. US competitors are at ~2x and they are far inferior businesses in my opinion. So there are several turns of multiple available on a re-rating once the market starts to see where this going.

Yes, CRON’s cash is drag on the equity, but as noted, given the currently depressed valuations and all the opportunities to deploy capital in the industry, it’s not remotely a tall order for the company to deploy this cash accretively. Create anything more than $1 of value for each dollar deployed, which should not be difficult, and the upside comes quickly.

What would I pay for companies with >25% topline growth rates, operating leverage, no cash burn, multi-decade runways, fortress balance sheets, and a material chance of becoming global blue-chips in a burgeoning industry? Certainly more than 0.5x NTM’s sales and a large discount to NAV. A lot more.

***

I’ll conclude with the ultimate point. In my initial write-up, I pitched CRON as a net-net with vastly misunderstood competitive advantages and an underestimated runway that would be lifted to glory upon the turning of the capital cycle. My thesis remains in tact, but with a pleasant caveat: we did not need the capital cycle to do the lifting. I clearly underestimated the quality of this business, with the last five months demonstrating that it is not only built to withstand this violent cyclical downturn, but that it is robust enough to thrive during it. The progress Cronos has made in the midst of this horrendously irrational competitive landscape is truly impressive; once the cycle does turn, I think the sky’s the limit.

Quality, growth and a long runway….at deep value prices. Count me in.

Disclosure: I am long shares of CRON and OGI

And that’s fine, it’s just going to kill off the weak hands faster

Thanks for the update!

A lot of people still see these companies as un-investable, as the excise tax is a huge hurdle for the business model. I hope Canadian government wakes up sooner than later, but they have a pretty shitty track record of fixing things before they get really ugly, so I wouldn’t be surprised if it takes longer than expected.