Actionable Ideas Update

Actionable Ideas Update

And a welcome to new subscribers

Disclaimer: Nothing on this blog is intended as financial or investing advice. Please do your own due diligence.

***

After launching an X/Twitter account last week (for anyone not already doing so, you can follow me at @ragingbullcap) this blog received an influx of new subscribers, largely due to excitement around my Cipher Pharmaceuticals write up from last month.

First of all, a warm welcome and thank you to those new subscribers. I hope you will find the content moving forward informative, thoughtful, and helpful for idea generation. I would encourage you to check out the About section of this blog for some further information about me and what I am looking for in an investment. You will also find a Table of Contents on the home page to help you navigate. Though this blog is very much still in its infancy (I launched it about two months ago) and will likely evolve over time, what you can expect moving forward are two varieties of posts: 1) actionable investment ideas, all of which I will have an economic interest in unless otherwise specified (and material updates of those ideas) and 2) quarterly updates of my personal portfolio, which will include commentary on positions I hold but have not written up (either because I have not had the time to do so or because I no longer see them as interesting enough to warrant a write-up) as well as some musings on the market and value investing more generally (you can see an example of this in my 2023 year end post here).

So far, I have written up 5 ideas on this blog, all of which still remain actionable to varying extents. Given many of you have just arrived, I figured I would provide brief summaries and updates of those ideas here to bring everyone up to speed.

Nuvation Bio (12/14/2023 - (+28%))

Nuvation Bio is a balance sheet investment with the free optionality of successful pipeline development. At the time, I described it as a “heads I win, tails I win even more” set-up. As of its last quarterly report, the company held c. $620mm of net cash (no debt) or $2.82/share vs. a share price of $1.37 at the time of the write-up. The company also had only one clinical stage drug (NUV-868) left in its pipeline (Phase 1 trials still ongoing) and a DDC platform, for which I ascribed no value. The investment thesis was simple — a binary decision tree in which either outcome was likely to increase the share price. In the first scenario, NUV-868 would fail its Phase 1 trials, in which case we would be left with essentially a cash shell (which we purchased at less than 50 cents on the dollar) and the company would likely pursue strategic alternatives, which would likely be shareholder friendly given large insider ownership and a plethora of high-profile institutions on the register. I posited one likely outcome of a strat. review to be a liquidation and conservatively estimated liquidation value to be $2.20/share (i.e. after subtracting quarterly burn and winddown costs from the cash balance), good for a +60% upside at the time of posting. In the second scenario, Phase 1 trials for NUV-868 would be successful, which would likely re-rate the stock, providing unquantifiable, though likely material upside on which we could “sell the news”.

Since the write-up, there has been one material development, which is that the FDA cleared the company’s IND to evaluate the first candidate from the DDC Platform, NUV-1511. This development, which was considered in write-up, is both a positive and negative depending on how it is viewed, and net-neutral in my opinion. The positive is that it suggests some value for the DDC Platform (which I attributed no value to) and provides the company with another shot on goal from a pipeline perspective. On the other hand, any success for NUV-1511 could delay a strategic review and increase cash burn (thereby eroding liquidation value). While cognizant to avoid thesis drift (this is not intended to be a speculative biotech bet, but rather a claim on the large cash balance with an option on the pipeline) I don’t think we have reached that stage yet. For one, NUV-1511 is in very early stages and not likely to materially impact cash burn at this point. Further, as I noted in the write-up, I think it is unlikely the company moves forward with the DDC Platform candidates if NUV-868 (which is clearly the lead program) fails. Therefore, I do not think the odds of the company “throwing in the towel” are materially impacted by this development and I think that the data readout for NUV-868 (expected sometime in H1 2024) is likely to be good for shareholders whether successful or not. Despite the 28% run up in the share price since the write-up, there is still a large margin of safety given the large discount to net cash and this is still a good asymmetric bet in my opinion, though I obviously liked this a lot more in the $1.30s.

Tidewater Midstream (12/21/2023 - (-14%))

This was pitched as a special situation, the thesis of which was rather simple: a (highly accretive) asset sale followed by deleveraging would lead to a significant re-rating of the equity, with further upside available through capital returns and additional asset sales (which were likely given the sizeable and persistent SOTP discount).

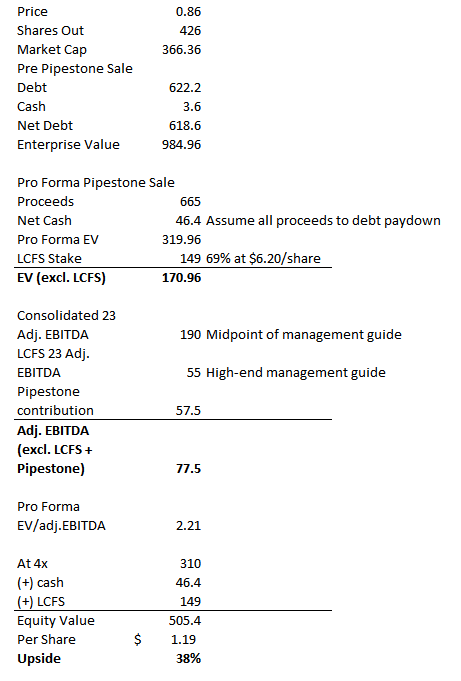

Early on, the situation unfolded precisely as I laid out. The sale of the Pipestone asset for $650mm (11x EBITDA) closed before the New Year, and shortly thereafter, the company announced that it had fully monetized the stock portion of the proceeds and initiated a buyback in lieu of the dividend. Everything was unfolding as expected and the stock went from $0.98/share to as high as $1.08. But, alas, nothing ever goes that smoothly, and on Jan. 22 the company suddenly and surprisingly replaced the CEO (who was doing a phenomenal job IMO), CFO and a board member. The move was clearly motivated by acrimony — the customary praise for the departures was altogether absent from the press release. Obviously, a move like this is concerning, particularly given the company’s history of poor execution. That said, it is equally possible this move was done in the interests of shareholders - e.g. perhaps there was some impropriety going on behind the scenes we are not aware of. Given the presence of two large private equity shareholders, one of which is currently occupying the Chairman’s seat, I am cautiously optimistic that there were good faith reasons for this shake-up. That said, the market has taken a “shoot first, ask questions later” approach and the stock has sold off to around $0.86. It is not possible to disentangle how much of the sell off is attributable to the managerial change, vs. the sizeable decline in LCFS shares (TWM’s 69% ownership constitutes a good amount of its SOTP value), given that LCFS shares its management with TWM, and therefore may be selling off for the same reason.

With all that said, I am trying to not lose sight of the forest through the trees. The reality is that TWM was once a substantially levered company that now has a net cash position and is incredibly cheap both with respect to its earnings power and asset value. After subtracting the LCFS stake, the remaining business trades at only a little over 2x my estimate of adj. EBITDA. Applying a 4x multiple and adding back the cash and LCFS equity, TWM should be worth around $1.20/share. Here is the math:

I would note that I think this valuation likely understates the upside, as LCFS is currently trading at an all time low and should hopefully begin to trend up once we get some clarity on the managerial shakeup. Indeed, LCFS shares were trading for around $10/share just a few weeks ago. At that valuation, TWM’s stake is worth ~$240mm which implies a share price of $1.40/share based on my model, or a 60% upside. As I have noted elsewhere, the present structure between TWM and LCFS makes no sense, as TWM’s ownership ties up so much of the LCFS float and makes the latter’s equity virtually unownable (ADV of c. 7000 shares). Previous management intimated awareness of this issue and I am hopeful the new management team will look for ways to monetize TWM’s stake, which would be beneficial to the shareholders of each entity.

My best guess is that TWM shares should begin to trend towards fair value once earnings are reported next month, as the stock will begin to screen with a net cash balance and management will have the opportunity to update shareholders and articulate what the plan is moving forward. It simply should not be trading for less than it was before the Pipestone sale was announced. Despite the uncertainty, I really like the risk/reward here as the stock offers a huge margin of safety below $0.90/cents and is currently priced for peak pessimism; there are a lot of ways to win here and any good news should send shares higher.

Sportsman’s Warehouse (01/14/2024 - (-7%))

SPWH is a retailer which I believe is ripe for a turnaround in the coming quarters provided it can return to my estimate of normalized margins. I believe this turnaround is likely because: a new, highly qualified CEO has taken the reigns and so far has said all the right things; operating margins are set to improve as the company has changed course and decided to not built out any new locations in 2024 and cost reduction measures will begin to show through as one-offs like severance fall away; the company has already guided to reduced inventory levels; the working capital benefit will be used to paydown the debt; and there should be a demand tailwind for firearms and ammo as the the 2024 Presidential election draws nearer. At $4/share, the stock is extremely cheap. I estimate the company can do $1.36 of EPS if margins normalize, implying the stock is currently available for less than 3x normalized earnings. Based on comps and an assessment of business quality (the company has historically generated high-teens ROICs), I think the stock is worth at least 6x P/E, or at least a double from here.

The stock trades with a fair bit of volatility, and I am taking the opportunity to buy dips below $4/share. Absent some material event, I don’t expect the stock to do much until the company reports next in April.

Instil Bio (01/25/2024 - (-2%))

This is a deep-value situation with what I believe to be a likely strategic review announcement in the near-term that should serve as a catalyst to close the large NAV discount.

Instil is a busted biotech. Over the course of the last year, the company has discontinued its lead drug program, announced several RIFs (leaving the company with very few employees), and more recently, outsourced its remaining candidate to a Chinese company and closed its UK facility. Effectively, what remains is a large cash balance (c. $185mm) and the ownership of a brand new 128,000 sqft property in Tarzana, California and its accompanying mortgage, available at a market cap of c. $75mm. The company recently noted an impairment of the real estate and marked the value at $132.5mm, implying an equity value of c. $50mm after accounting for the $83mm mortgage. There is reason to be highly skeptical of this figure, as I explain in my write-up. However, even under the absurdly punitive assumption that the real estate has zero value and the company would have to satisfy the mortgage in full with its own cash balance, we would still be buying shares at a discount to the remaining cash. Under a more reasonable assumption that the equity value in the real estate is zero, but that the asset covers the debt, then shares currently trade for around a 55% discount to NAV. Therefore, any equity in the real estate at all is simply a bonus. Given the company has virtually no operations left, and that it has listed the Tarzana property for lease and sale, I expect there will be an 8k in the near-term announcing a strategic review, which should help close the discount in part. I do not trust management here at all given the track record of destructive decisions (a pre-revenue biotech funding the development of a ~$100mm state of the art facility…seriously?), but given how enormous the discount to NAV is here and considering how much equity management owns, I am comfortable with that reality.

Cipher Pharmaceuticals (01/31/2024 - +30%)

I will direct you my recent thread on X for a summary of this situation. This is up a bunch in the weeks since I wrote it up, but I think we are still in the third inning on this one and the risk/reward is just incredible in my opinion. I have continued adding shares into the $7s.

***

Please feel free to reach out here or on X if you have any questions or comments and thanks again for subscribing.

Cheers,

Also: Do we know anything about the status of the NCIB? Are they buying back opportunistically under a specified price point, or just purchasing x % of float per day? Thanks.

Hey Jake, I have begun my work in the last two weeks diving into CPH.TO as well... quick question regarding the perception of MOB-015. From what I've seen, we will likely have Phase III completed in Q1 of 2025. Given the fact that markets are typically 9-12 month forward looking instruments, it would appear that CPH is being valued like the market is not optimistic of this outcome. Do you think this is the byproduct of the security not screening well? Being a microcap / less explored asset class? Or do you feel that it's also the market simply disagreeing that MOB-015 will gain clearance ~1 year out? Would love your thoughts, thanks!