Idea Update - 2/3/2025

ZEG.L, ENZ, NOL.OL, BQE.V, CRON, MREO

Disclaimer: Nothing on this blog is intended as financial or investing advice. Please do your own due diligence.

Zegona Communications

This one has been a home run so far (and fortituously timed), up 55% since my write up before Christmas. The re-rating has been driven by a successive string of positive developments that have a gone long way towards proving out the thesis.

First, Zegona provided its first financial update for Vodafone Spain since making the acquisition. Impressively, in the first full Q under Zegona’s control (ended Sept.) Vodafone has already shown marked improvements in profitability from the preceding Q (ended June). While revenues came down slightly from 916mEUR to 903m, EBITDaL improved 6% to 318m, and EBITDAaL - capex increased 23%. That’s a small window to draw firm conclusions from, but that clearly improved efficiency is a great sign and will be a huge driver of equity value if sustained given all the leverage on this structure. This should be augmented by expected pricing increases in the industry this year and several other levers yet to be pulled.

Next, we’ve had a couple positive developments on the fiberco spin-off front (recall, a pivotal part of this thesis is Zegona monetizing these fibercos at a premium multiple and using the proceeds to deleverage — hopefully raising sufficient capital to fund a special dividend sufficient to redeem the Preference Shares, with the outcome tantamount to a repurchase of nearly 70% of shares outstanding at hugely discounted 150p/share).

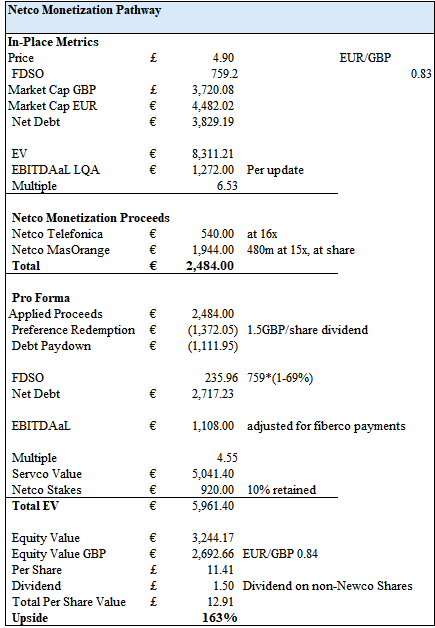

The first update on this piece came in early January with the finalization of the larger MasOrange fiberco deal (now named “Surf”). With this announcement, we got our first comment from the company on the JVs prospective earnings power, which the PR pins at ~€480 EBITDA in three years. That’s actually materially higher than the €420m I estimated in my analysis, particularly given the high multiple warranted on those earnings.

Then, last week, Bloomberg reported that bids for the smaller Telefonica fiberco (now named “Milos”) have come in. The reporting notes that four non-binding bids were received, including from Armancio Ortega’s Pontegadea, who is apparently the most likely winner. Notably, the reporting also indicates the 40% third party stake is expected to be worth 800m-1B EUR, which implies a 16-20x EBITDA — higher than the 15x I used in my underwriting. Using 16x, Vodafone’s 37% stake is worth 740m, and they would receive gross proceeds of 540m by selling their stake down to 10%. Finally, the reporting notes a final agreement should be expected by the end of spring/early summer.

Collectively, these developments go a very long way in derisking and proving out this thesis. And, in my view, the stock remains extremely undervalued despite the big move recently (and what has already been an incredible return for an LBO that closed in May with a 150p/share equity placement).

Here’s my udpated underwriting, starting with today’s share price, on the value that can be unlocked simply from monetizing the Netcos and applying the proceeds to deleveraging, and using the updated EBITDAaL and Netco figures:

[Feel free to pushback]

That output is nearly 100% higher than my original underwriting, which is an unsurprising product of an EBITDAaL figure running 15% higher than the provided 2023 figure, and increased profitably and multiple estimates for the Netcos, getting magnified by a tremendously levered capital structure. Maybe I am too optimistic in one place or another - e.g. you could aruge I am being premature in simply annualizing last quarter’s EBITDAaL, (although on that piece I’d note that this figure is still well short of the 320mEUR of savings management expects to achive from the acquisition date, which would actually result in >1.3B EUR of EBITDAaL if achieved). Also, it’s essential to remember there’s a 15% promote on upside to the market cap from ~2.4B GBP which will drag on our returns. Regardless, the point is there is a lot of upside from here if all goes according to plan without any crazy assumptions. Further, I am only valuing the opco at ~4.5x above; the math really gets crazy, pro forma the above deleveraging, if you assume a higher multiple at exit; indeed, it’s not hard to arrive at >£20/share of total value when this is all said and done.

So far, this has been a really fascinating case of mispricing attributable to an unsual public markets vehicle, a London listing, and a complicated capital structure with no investor relations effort to help one make sense of it. Not to say this ends up successful in the long-run, but it’s a good reminder of the virtues of looking where few others are.

Enzo Biochem

From a home run to a total stinker. Enzo has served as a frustrating reminder of the old Buffett adage that “time is the enemy of the mediocre business” (medicore might even be a charitable descriptor here). This one is down ~30% after accounting for the special dividend.

When I wrote this up back in May the thesis was simple: a large SOTP discount with the downside protected by tangible asset value and some pretty strong incentives to unlock the value and wind things down.

I flagged four risks at the end of the write up:

Risks 2 and 3 are more general in nature/and sort of redundant, but incredibly each of those four risks have materialized. The two specific risks — the ransomware litigation and opco regression — are worth some reflection.

On the ransomware issue, I canvassed some prior precedents and noted that $10m appeared to be the worst case outcome. Last month Enzo finalized the settlement of the relevant class action for $7.5m, which alone was near the high end of my bear case. However, Enzo was also forced to settle with certain state Attorney’s General for more than $6m, which brought the cumulative ransomware liability up to nearly $14m, or nearly 50% higher than my worst case assumption, and more than 25% of the market cap at the time. That put a substantial dent in the SOTP math and our tangible downside protection.

Notwithstanding, that alone might not have been enough to cause us impairment. However, just as the extent of the expanded liability was beginning to emerge, ELS (the opco) put up a terrible Q125, with revenues declining 20% YoY. While generally one weak quarter is not enough to meaningfully impair value, the sudden drop indicates that ELS’ string of strong quarters was likely a false alarm and that this business remains cyclical, commoditized, and likely susbcale in perpertuity.

This in turn suggests that my bear case revenue multiple of 1x is likely fair (or even too high?), and with a melting balance sheet, that 20% hit to the opco’s value stings.

Again…time is enemy of the mediocre. Unsurprisingly, Enzo has long been a case study in this lesson. The stock has been written up 3 times on VIC dating back to 2010 and each successive pitch at a lower price than previous: $10.50, $5.82, $2.12. Add me to the long list of suckers at $1.05. Any takers at $0.60?

The two aforementioned impairments have occured alongside some very perplexing behavior from the C-suite. What pushed this from cheap, to investible, for me initially, was what I perceived as very strong incentives/alignment from insiders to wrap this up promptly. And subsequent behaviour only strengthened my conviction there, including CoC compensation amendments and a sizeable slug of options for the CEO (and the CFO) at a $2 strike. That has made some of the more recent behavior/decision-making strange.

First, at the end of the year the company announced a 10c special dividend (~10% of the market cap). While that was initially well received (I it interpreted it as a signal that a bigger strategic transaction was underway and that the thesis was even more likely to work out), its puzzling that the company would return 10% of its cash to shareholders right before a meaningful decline in PnL and acceleration of cash burn, with seemingly no plan in place. Moreover, why push your options struck at $2 further out of the money by paying out a large dividend rather than, say, doing a tender? In retrospect, it may be attributable to an internal abandonment of any expectation that we’d ever get anywhere near $2.

Beyond that, the company still has not announced a stragetic review or communicated any path forward. I frankly find that disrespectful to shareholders, particularly given it has become clear that ELS is never going to scale sufficiently to cover corporate costs and therefore, the balance sheet will continue to melt until some corporate action is taken. Time is ticking.

Putting that altogether, I am not at all surprised the stock is now at 60c. But is the capitulation over done? Maybe.

At 60c, the fully diluted market cap is ~$31m. For that, here’s what you get:

$32m of net-current asset value as of Oct. 31 (this includes a full provision for the class settlement), including ~$48m of cash. That will come down with subsequent burn, but it’s less than $3m per Q even with the lower revenue, and ~$1m if revenue can trend back up.

Real estate worth $10m at cost and likely closer to $15m at fair value;

An operating business worth $25m if you annualize last quarter’s sales and value it at 1x;

And >$78m of federal NOLs, worth ~$16m undiscounted (and some state and local NOLs as well).

So you’re effectively buying the cash and near cash equivalents, and getting the business, real estate, and some interesting tax assets for free. Enticing, but it’s only a little better than the discount we created in May and look how that turned out.

One material difference, however, is that the two specific risks I identified are largely out of the picture. The ransomware liabilities are paid, so the left-tail litigation risk is gone. And while the opco could always deteriorate further, it’s worth noting ELS’ revenues have been range bound going back a decade plus, and last Q annualized marks the bottom of that range. That doesn’t mean it can’t go lower, but there’s a good argument this is just the same cycle as its always been.

The most interesting piece, however, is the NOLs. In November, the company appointed Jon Couchman to the board. Couchman has an interesting and extensive history with winddowns, including literally holding the title as “Chief Wind-Down Officer” at a company called Footstar in 2009. His initial statement of ownership with Enzo indicates preexisting ownership of ~450K shares held by various entities. I took the onboarding of yet another guy with special situations experience with decent skin in the game, immediately after the announcement of a large special, as a clear signal that some larger corporate transaction was about to take place. That turned out to be a massive head fake given the stock’s collapse two weeks later. But digging a little deeper into Couchman one quickly discovers that he has a penchant for structuring (or at least attempting to structure) transactions to monetize substantial NOLs: see e.g. here, here, and here. This piece explicitly lays out his approach, and its worth including some excerpts:

Beyond concluding that Couchman was likely brought in to ‘monetize’ the NOLs/structure a transaction to preserve them, it’s anyones guess how this plays out. This piece of the story does, in my view, support an inference that management has given up hope in getting much, if anything, of value for ELS (though not necessarily). The IRS’s rules around NOLs are complicated, but an important piece to understand is that they broadly cannot be acquired. As such, a deal would need to be structured whereby Enzo acquires a business that could benefit from the prospective tax savings. Focusing on just the federal NOLs (as of the last 10k), Enzo has ~$78m, which are worth ~$16m at a 21% tax rate. Notably, most of these do not expire. In many cases, NOL structures involve liquidated shells, which complicates the ability for the shell to finance an acquisition (see the linked Couchman articles above). Here, however, Enzo has nearly $50m of cash that can be used to acquire a profitable business that could have its income taxes wiped for years. In turn, the acquisition could add scale and more segment level income to spread across fixed corporate costs, making ELS’s contibution more valuable. Altneratively, ELS could get sold, adding more cash for another acquisition.

In short, there’s a multitude of ways this might play out from here, but I think it’s likely to be along those lines. It’s actually quite an interesting set up, in my view, and with cash burn likely to be low given the cleaned up liabilities, I don’t think you’re taking on much risk here to find out (I know I said the same thing 35 cents higher).

With that said, investors need to be aware of a few other pieces. First, the company is non-compliant with its NYSE listing due to its market cap/book value declining below $50m, and its share price trading below $1; they can cure the share price issue through a reverse split, but getting compliant on the market cap/equity deficiency is another story. Accordingly, this very well could trade OTC and go dark at some point; indeed, that’s been the trajectory of Couchman’s prior episodes and its not far off from how the company has been operating in recent years. I.e. the company may welcome a delisting.

And that ties into the next piece — which is that the MO in these situations tends to be precisely this: going dark on communication, flushing out bag holders, and insiders eventually taking control, with the shares eventually going OTC/expert to save on costs.

And finally, timing. It appears that some of Couchman’s previous efforts with these shells have taken forever to unfold: e.g. the Myrexis shell seems to have been sitting dormant for over a decade now; likewise with the coincidentally named Enzon, which has been purportedly looking for a deal for 5+ years (with a very similar cash balance to ENZ, and apparently Carl Icahn as a shareholder). The very real difference here, in my view, is that ENZ still has a material operating business attached to it, and several 13d/g filers that surely do not want to sit around forever with capital tied up here.

Ultimately, this is now a very different thesis, but an interesting one to monitor if gamey nanocaps are your sort of thing. If anyone has thoughts on this setup that I might be missing, on Couchman, etc. I would love to hear them.

Northern Ocean

This one’s returned ~10% thus far, though it has come down a lot. I am in “proceed with caution” territory at this point.

Since my write up in October, backlog has increased from <$100m to over $500m. This has been driven principally by a $400m contract with Equinor for Deepsea Bollsta for a firm duration of two years commencing in H2 25, with five one-year options. This award, at an implied $460K/day rate, is awesome news for the company. At 90% utlitization, that’s ~$85m of Rig level EBITDA annually for an asset being valued at ~$320m at today’s share price.

The problem is that NOL needs both of its rigs working to generate cash flow, and despite Total excercising an option for Mira for an additional 2-3 months at an attractive rate, that rig remains without any work looking beyond the spring. That very well could change, and I think the odds are quite good (the market in Norway has been strong and there’s not a lot of spare HE semisub capacity), but the whitespace is certainly a risk, particularly given >$80m of interest and principal due this year, and all the debt maturing in 2026. The path ahead is for the company to refinance its debt, perhaps tapping the bond market, but that ambition is imperilled if they can’t secure sufficient backlog and get Mira working.

Of course, if Mira can get anything resembling the contract Bollsta receieved, this investment likely turns out very well. Having both rigs operating at $450k rates results in EBITDA net of corporate costs of ~$170m, which puts us at merely 3.7x EBITDA. Moreover, even with the high cost of debt and after maintenance capex, those rates amount to a >35% levered free cash flow yield, which will drive a huge re-rating of the equity as that FCF delevers the balance sheet.

In sum, I continue to find the risk reward very compelling.

BQE Water

Not much to say here, but I’ll flag three notable developments:

Renewal of the buyback authorization was secured in December for up to 5% of shares. I don’t expect any buybacks to be conducted at today’s share price, but my understanding is they want to be prepared for any silly and percipitious drops like we have seen in the past. I really like this management team, but I’ve encouraged them to worry less about the stock’s liquidity when it comes to buybacks, and more about capitalizing on any opportunity to buy out partners at a discount to intrinsic value; the trade will trade better as a function of growing earnings per share, not the number of shares outstanding. The reality is that BQE is starting to pile up quite a lot of cash and they have very little need for it. That’s the beauty of a cash-generative, asset light business, but the growing cash balance is at some point soon going to compel management to do something with it, lest it starts being an anchor on the equity. Capital returns are likely not as far away as one might think.

BQE appears to have consulted on a SART plant in Mexico for GoGold. Looks like a fairly sizeable project that could be a recurring revenue contributor in time.

Finally, it’s worth noting the significance of gold blasting through all time highs. This obviously spurs mining activity, and in turn, the size of BQE’s potential pipeline. Most immediately, a sustainably high gold price makes it increasingly likely that the KSM company-maker project gets financed, which, you might recall, could on its own double recurring revenue.

Cronos Group

Again, not a lot to say on this one other than to reiterate my endless astonishment as to how cheap this is. The stock is at $1.85 as I write this, so the market cap is ~$700m. For that, you get: $860m of cash, a $16m loan receiveable, $47m of inventory, $20m of AR, a $9m facility held for sale, ~$13m of other receiveables and prepaid assets, and $162m of PP&E. In sum, that’s $1.1B of tangible assets against $53m of total liabilites, which nets to nearly $2.80/share in tangible book value. Just using current assets, this is a net-net at $2.38/share in NCAV.

Cronos is not the only net-net you’ll find in the market, but it might be the only one I have ever seen that is growing top line 30% annually, burning zero cash (in fact, NCAV is growing), rapidly expanding margins, owns the #1 brand domestically, and has a stunningly long runway. Net sales in the NTM should be well over $140m and that’s after the wildly punitive excise tax. Meanwhile, margins will continue to expand as domestic pricing trends up and the export business (which is excise tax exempt, and thus higher margin) grows. Net-net status is usually reserved for dying businesses or cash incinerating ones — this is quite the opposite.

I know a lot of investors are getting fed up with the cash not being put to use, and part of me agrees with that sentiment. With that said, I don’t see any rush — there continues to be a lot of uneconomic, subscale players still damaging market dynamics— and I appreciate management’s restraint in not doing M&A simply for the sake of it. In many ways, I think CRON is best viewed as two business: 1) a growing cannabis producer with a strong brand and substantial share in the world’s most developed cannabis market and 2) a cannabis SPAC, clipping a yield on its cash waiting for a fat pitch. At $1.85, we aren’t paying anything close to fair price for either of these.

I am hoping to do a deep dive on OrganiGram in the coming months, and will have more to say about my broader thoughts on cannabis then.

Mereo BioPharma

I continue to like this set-up despite some tough price action recently. The sell off has been driven by two things.

First, lead drug setrusumab did not meet the stringent p-value necessary to hit at the first interim analysis in its ongoing P3 trials. While that would have been a welcomed result, very few people (including management at both RARE and MREO) thought the odds of success this early were very good. As such, I am somewhat surprised by the reaction to the news, although it makes sense when you consider that a lot of traders were likely looking to play the first interim as a trade, and have exited given we are now months away from another catalyst. Again, the first interim was always a major long shot, and I continue to think the odds of the second interim are much higher. Here is what the RARE CEO had to say in response to a question about the PoS being impacted by falling short of the first interim:

The second interim is scheduled in Q2 this year. If successful, I think shares could more than double from here (some of the sell side numbers have it much higher than that). If not, the pivotal final analysis should come in Q4, at which point this thesis becomes far more binary and worth reconsidering.

The second, and more frustrating issue, has been the failure to secure a partnership/financing deal for alvelestat, despite the CEO’s frequent communication that the program would be ready for phase 3 by end of 2024. In my view, this is much more of an issue than the setrusumab one. Great assets generally should not take this long to transact, especially given some of the crazy valuations for similar products I discussed in the write-up. From my view, the CEO’s excuses for why a deal still hasn’t been done are getting stale and filibuster-y. In the most recent update, she noted that the recently secured Orphan Drug designation is “another important milestone in our ongoing partnering process and our efforts to bring alvelestat to patients worldwide”. That is probably true, but it doesn’t particularly excuse falling short of your long communicated timeline. And the issue for investors is that getting some value for this asset in advance of the setrusumab readout was always a big derisking piece that made this a unique biotech investment, with less binary risk. The longer this drags on, the more clinical trial risk we face.

With all that said, I continue to hold given the high PoS of setrusumab clearing the second interim and thus derisking this well before the final analysis. Moreover, I am still optimistic something will come of alvelestat, or perhaps a larger transaction selling the entire company, given the smart money in the stock and Rubric’s presence on the board.

***

No updates for JBGS, CPH.TO, and RDI

What is your opinion on the impact of a potential Canadian goverment change for Cronos?

I would argue that it might be short-term slightly negative, long-term beneficial.

My base case for a Conservative government would be to keep the excise tax as is. Given their problematic relationship with cannabis in the past, I don't expect any pro-cannabis changes to be made, but it would be fiscally irresponsible from the budget perspective to try to harm the industry.

This could prolong current market conditions, where:

1) Smaller, weaker producers could cease operations, limiting the amount of oversupply

2) Reducing cash burn is key, which Cronos has already done

3) Lead to market consolidation, where strong balance sheets are even more valuable

In the long term, a highly punitive excise tax might cleanse the cannabis market, reducing oversupply and competition. If after a prolonged period the excise tax is lowered, this could then act as a torque for Cronos. I am not a Canadian though, so curious to know what is your opinion.

Thank you - great post. Always enjoy your writing!