TWM.TO Update - 1/9/2024

TWM.TO Update - 1/9/2024

AltaGas shares monetized; LCFS on a tear

Disclaimer: Nothing on this blog is intended as financial or investing advice. Please do your own due diligence.

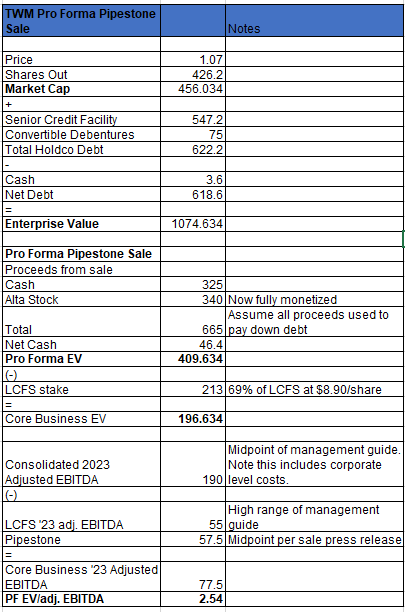

Another brief update on the Tidewater Midstream situation. Recall that the Pipestone sale proceeds were approximately split 50/50 cash and AltaGas stock. In the initial write-up, I credited the proceeds as entirely cash when underwriting the pro forma capital structure, but I noted it might take TWM some time to fully monetize the shares due to limited liquidity. Well, the company managed to unload those shares faster than I anticipated, announcing today the entirety of the AltaGas shares have been sold for proceeds of ~$340 million. Great news obviously, as the company now has a net cash position and ample liquidity to both paydown debt and execute the buyback program.

As a cherry on top, Tidewater Renewables (LCFS) (which TWM owns a 69% stake in), has been on an absolute tear since I published write-up, closing out the day at $8.90 vs. $7.31 (up 22%). This implies TWM’s stake is now worth ~$213 million. This increased equity holding is material, given that the LCFS stake is worth more than half of TWM’s pro forma enterprise value. I did not underwrite any increased value for LCFS, so this is simply added upside for the thesis.

Altogether, there have been four noteworthy and bullish developments since publication: 1) the closing of Pipestone, which was the key catalyst; 2) announcement of a share repurchase program, which was not part of the thesis, but is obviously welcome; 3) monetization of the AltaGas shares, which happened more quickly than I expected; and 4) a big run in the renewables subsidiary, which was not necessary for the thesis, but is a significant value-add.

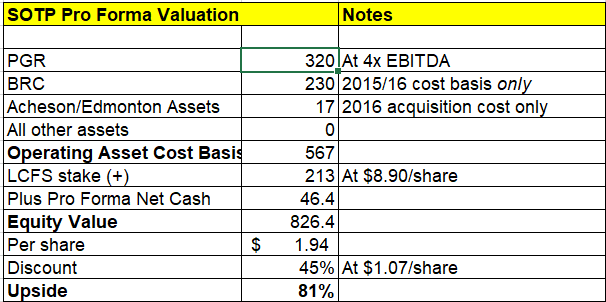

The stock jumped on today’s news, closing at $1.07, up ~9% since the write-up. In my opinion, this move is not nearly enough and the price is still way too cheap. In fact, the remaining operating business is currently being valued just as cheaply on an EBITDA multiple as it was at the time of the write-up - i.e. 2.5x EV/adj. EBITDA - given the LCFS appreciation.

If we apply a conservative 4.5x multiple to the operating business, I get to $1.43/share or 33% upside in the near-term. And that’s before giving any credit to the buybacks. However, as I said in the write-up, I think this is set to go even higher in the medium-term. Management is proving themselves to be prudent capital allocators and are clearly doing everything they can to drive shareholder value. The stock still conservatively trades at a 45% discount to my SOTP math, and I expect further assets will be sold in short order to get us there.